The insurance industry, traditionally known for its rather cautious, conservative approach, has experienced significant changes in recent years, adopting new digital technologies in response to consumer demands and market dynamics. However, leading analyst firm Gartner recently cast a shadow of doubt on this progress, declaring, “Insurer progress with digital is typically overstated and does not match the reality.”

This raises the question, how digitally advanced are insurers? And how prepared are they to tackle the next frontier of new technologies around AI and automation?

In this article, we explore how much progress has been made, how the insurance industry compares to other industries, and the future outlook for 2024 and beyond.

The State of Digital Progress in the Insurance Industry in 2023

Over the past few years, insurers – who had long been resistant to significant change – saw themselves forced to accelerate digital initiatives.

Research from KPMG indicates a substantial shift, with 85% of insurance CEOs acknowledging the pandemic as a catalyst for digitizing operations and spearheading new operational models.

Fast-forward to 2023, and it seems insurers are keen to keep up with the pace of change. According to Gartner, 43% of insurers are actively integrating Artificial Intelligence (AI) into their operations and 83% are expected to start using AI by 2025.

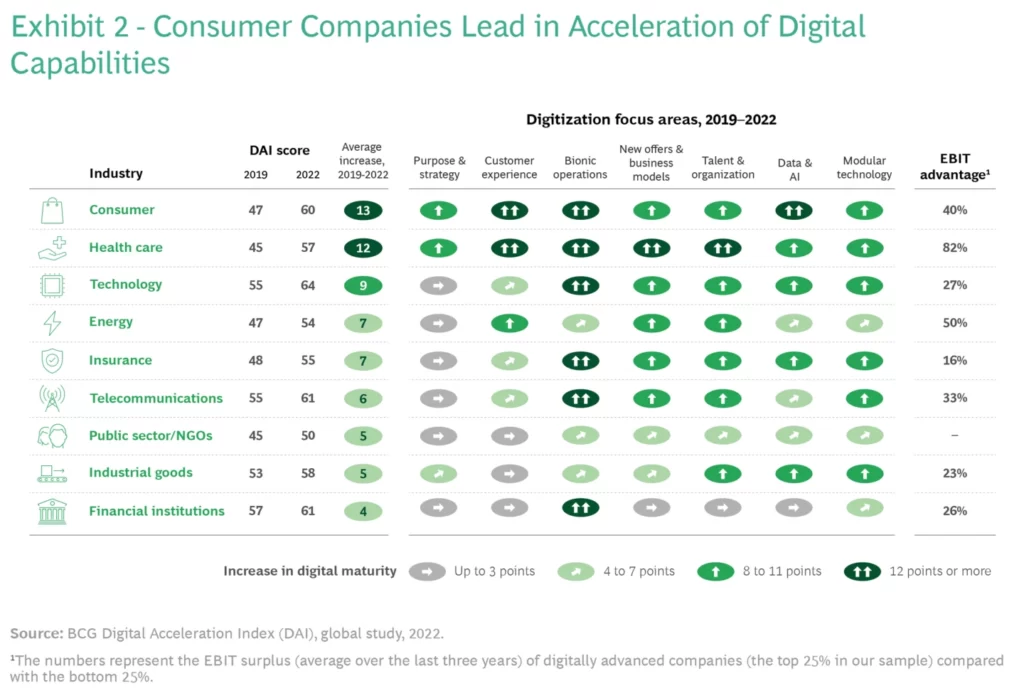

How Does Insurance Compare With Other Industries?

There is no denying that the insurance industry has made significant strides recently. But how does its progress compare with other sectors?

The BCG Digital Acceleration Index (DAI) assesses various industries based on their digital capabilities and readiness to integrate new technologies. Insurance managed to increase its score from 48 in 2019 to 55 in 2022. Despite the significant improvement, though, insurance still lags behind almost all industries, including healthcare, finance, and consumer goods.

More worryingly, the Earnings Before Interest and Taxes (EBIT) advantage is the lowest of all industries at 16%. The EBIT advantage metric refers to the EBIT surplus of the top 25% of digitally advanced companies, compared with the bottom 25%. The comparatively low score suggests that insurance companies aren’t deriving as much financial value from their digital initiatives as other industries.

That said, there are differences within the insurance industry, as company size is a key factor in digital maturity. A Gartner study found that 51% of insurance firms larger than $10 billion are currently leveraging AI, compared to only 34% of smaller insurers.

In general, data shows that larger insurance companies tend to have higher AI adoption, better levels of data and analytics leadership, and are more likely to possess organizational strategies as well as business and IT talent.

Digital Initiatives Have A Direct Impact on Revenue

So, insurers have partially digitalized their processes, but they are making less progress than other industries. Does it matter? Well, yes.

Adopting new technologies isn’t just about staying current: it impacts every area of the business, including revenue performance.

According to Gartner, half of the insurance companies that doubled down on their digital initiatives saw a clear increase in revenue. On the other hand, fewer than a quarter of companies that didn’t enhance their digital strategies saw similar results. This demonstrates the financial return for companies who step up and embrace digital transformation.

Overall, we are increasingly seeing a clear digital capability gap, splitting insurers into two camps: those rising to the occasion and those burying their heads in the sand. This strongly suggests that those who don’t step up will continue to fall further and further behind.

Today, digital capabilities play a more critical role than ever. Companies with higher levels of digital maturity are in a stronger position to tackle the top three challenges currently facing the insurance industry: economic pressure, talent scarcity, and supply chain shortages. Insurers need AI and automation to offset this triple squeeze.

For instance, according to news reports, inflation has spiked an increase in insurance fraud. Insurance companies with AI capabilities can use machine learning models to flag potentially fraudulent information during the claims process. Companies that are less digitally advanced will struggle to identify fraud, wasting human and monetary resources. This is why AI is no longer optional, or a “pet project” (if it ever was).

So, what can insurance companies do to boost their digital maturity?

5 Steps Towards Digital Maturity In The Insurance Business

Here are our top five strategic recommendations for reaching digital maturity and deriving the full benefits from AI projects:

• Prioritize Relevant Use Cases to Address Business Challenges

Choosing use cases that directly address key business challenges is essential to achieving a tangible impact with AI and other technologies. Identifying and implementing use cases that solve key business problems, such as improving customer experience or enhancing fraud detection, will ensure that AI investments are directed toward areas that will deliver measurable returns and drive value throughout the organization.

• Establish a Comprehensive AI Roadmap Driven by KPIs

Create an AI roadmap to navigate through the phases of AI integration in insurance operations. This roadmap should outline a deliberate, phased approach towards AI implementation, while the embedded KPIs ensure that all AI initiatives are precisely aligned with, and are actively driving toward, specific business outcomes. This ensures AI investments are closely aligned with organizational objectives.

• Go Beyond Data Analytics and Leverage Diverse AI Technologies

Insurers should expand their AI strategies to encompass more than just data analytics. Machine Learning and Natural Language Processing approaches, like Semantic Folding, have the ability to handle unstructured text and enable an array of new use cases. Insurers can leverage these technologies to speed up and automate document processing, saving time and improving accuracy in areas such as underwriting and claims processing. Furthermore, insurers should consider exploring generative AI to enhance conversational interfaces and chatbots.

• Cultivate Specialized Talent

Investing in the development and acquisition of skilled talent is crucial. Ensure your team can proficiently navigate through AI technologies and data analytics, thus ensuring not only the smooth adoption of technology but also fostering an environment that rewards innovation and strategic problem-solving.

• Put the Customer Experience at Front and Center

Converge technology and human elements to ensure that customer experiences are both automated and personalized. Leverage AI to efficiently manage and direct customer queries while preserving the essential human touch in high-value customer interactions, particularly in areas sensitive to customer experience.

Final Thoughts

The overall maturity of insurance companies remains a work-in-progress, with many gaps that need closing. Despite encouraging developments, the overarching reality is that comprehensive digital maturity is a goal still on the horizon.

Going forward, insurers must ensure that digital advancements are in lockstep with business outcomes, strategically embedding technology to solve business issues, boost customer satisfaction and drive revenue. By doing this, insurers will reap the full benefits of their digital initiatives and strengthen their market position.